For many online businesses, payment processing is one of the largest recurring operational costs.

Card networks remain dominant — but open banking payments are growing rapidly as a lower-cost alternative.

If your business processes large volumes of euro transactions, the question is no longer theoretical:

Should you continue relying on card payments — or switch to open banking rails?

This guide breaks down the cost structure, speed, security, and infrastructure implications of both models.

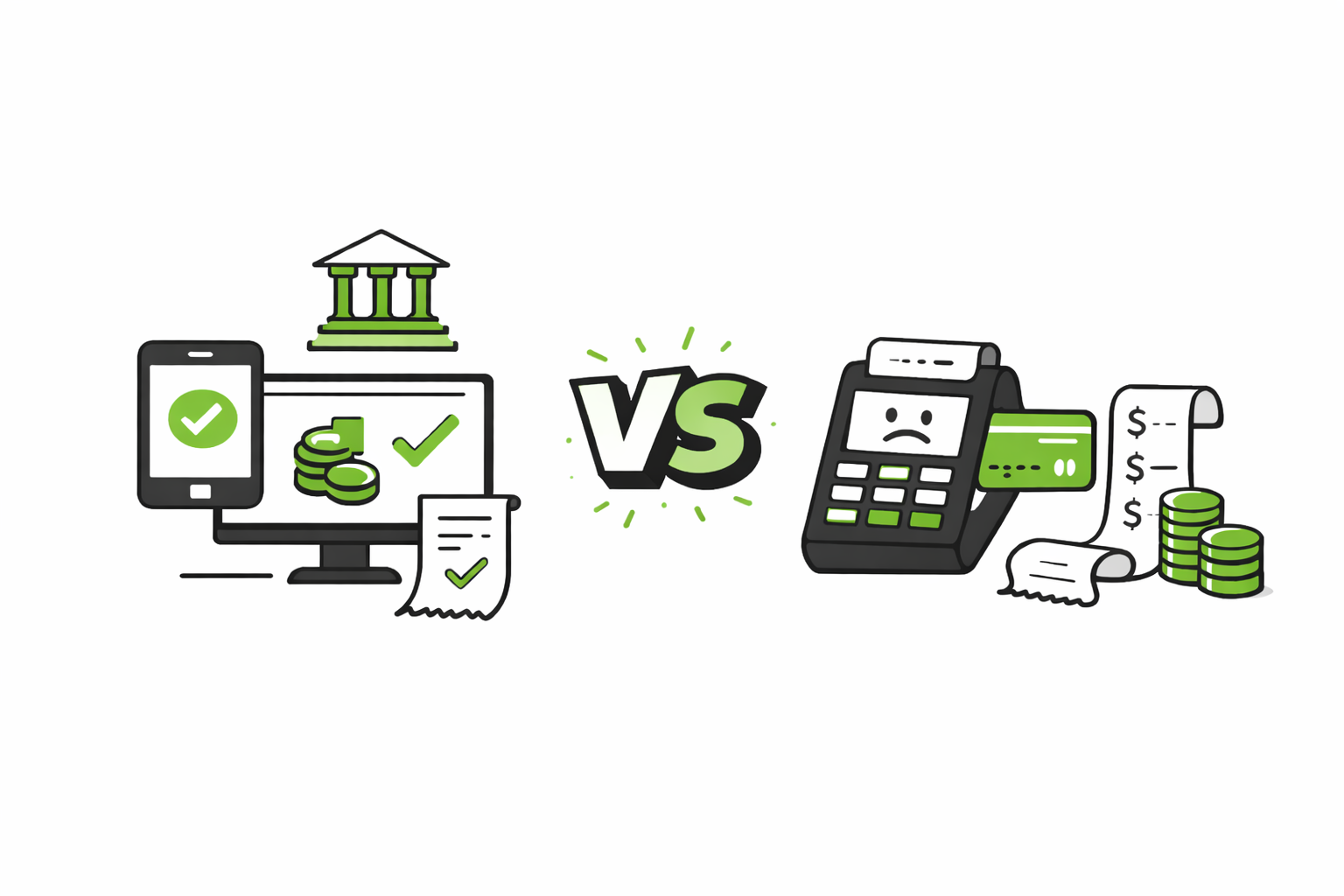

What Are Open Banking Payments?

Open banking payments are account-to-account (A2A) transfers initiated directly from a customer’s bank account.

Instead of routing through card networks like Visa or Mastercard, funds move directly between banks.

In the eurozone, these transfers typically run through SEPA rails governed by the European Payments Council.

Key characteristics:

- No card networks involved

- Lower processing fees

- Strong Customer Authentication (SCA) compliance

- Faster settlement in many cases

How Card Payments Work

When a customer pays by card:

- The card network processes the transaction

- The acquiring bank authorizes the payment

- Interchange and scheme fees are applied

- Settlement happens within 1–3 business days

Fees typically include:

- Interchange fee

- Scheme fee

- Acquirer markup

Total cost: often between 1.5% and 3% per transaction.

For high-volume businesses, that margin significantly impacts profitability.

Cost Comparison: Open Banking vs Card Payments

Factor | Card Payments | Open Banking Payments |

Processing fees | 1.5%–3% | Often significantly lower |

Intermediaries | Multiple | Direct bank-to-bank |

Chargebacks | Possible | Rare (push payments) |

Settlement time | 1–3 days | Same-day or instant |

FX fees | Applied on cross-border | Lower in SEPA |

For a business processing €2M per month:

- At 2.5% card fees → €50,000 in monthly fees

- At materially lower A2A cost → meaningful savings

Reducing payment friction directly increases operating margins.

Speed: SEPA Instant Advantage

Open banking in the euro area often relies on:

- SEPA Credit Transfer

- SEPA Instant Credit Transfer

SEPA Instant enables near real-time transfers 24/7.

Card settlements, in contrast, typically batch and clear through acquiring banks on a delay.

For businesses managing liquidity tightly — such as trading platforms or marketplaces — faster settlement improves treasury control.

Security and Fraud Considerations

Card payments are vulnerable to:

- Chargebacks

- Card-not-present fraud

- Stolen credentials

Open banking payments use strong bank authentication layers, often tied to the customer’s banking app.

Because they are push payments (initiated by the account holder), chargeback exposure is materially reduced.

This lowers:

- Fraud management costs

- Operational disputes

- Administrative overhead

Why Businesses Are Reconsidering Card Dependency

Card payments remain convenient, but several structural issues push businesses toward alternatives:

- Increasing scheme fees

- Margin pressure in competitive industries

- Higher fraud prevention costs

- Regulatory compliance complexity

- Delayed settlement

Open banking infrastructure reduces reliance on global card networks and increases control over payment flows.

Where Open Banking Makes the Most Sense

Digital Platforms

Marketplaces and SaaS providers benefit from lower fees on recurring billing.

Trading & Investment Platforms

Faster account funding improves user experience.

E-commerce with High AOV

Large transaction values amplify card fee impact.

B2B Services

Direct bank transfers align naturally with invoicing models.

Infrastructure Requirements for Open Banking

To accept open banking payments efficiently, businesses need:

- A dedicated IBAN

- SEPA connectivity

- API integration capability

- Batch payout support

- Compliance-ready onboarding

Fragmented setups (bank + PSP + treasury system) increase complexity.

An integrated solution simplifies operations.

How Monetum Supports Open Banking Payments

Monetum provides a unified euro payment infrastructure designed for digital businesses:

Core Infrastructure

Dedicated euro IBAN accounts for each business or brand

SEPA Credit Transfers across the Single Euro Payments Area

SEPA Instant capability for real-time euro settlement (where supported)

Open banking payment rails for direct account-to-account transactions

Batch payment automation for high-volume payout processing

API integration for platforms, fintechs, iGaming, and Web3 operators

What This Enables

This structure allows businesses to:

Reduce dependency on card networks and high processing fees

Accept and send euro payments via bank transfer rails

Automate bulk payouts in a single workflow

Improve liquidity and treasury visibility

Operate multiple dedicated IBANs within one platform

Centralize euro and crypto-related payment flows

For companies processing both fiat and digital assets, Monetum integrates wallet infrastructure and supports crypto-to-euro conversion (off-ramp) within the same operational environment.

Card Payments Still Have a Role

It’s important to note:

Card payments remain useful for:

- Consumer retail

- International card-heavy markets

- Subscription billing

However, for euro-dominated B2B flows, open banking often offers structural efficiency advantages.

Many businesses adopt a hybrid model:

- Cards for certain customer segments

- Open banking for cost-optimized flows

Regulatory Landscape

Open banking adoption has accelerated under PSD2 frameworks, enabling secure API-based banking integrations.

SEPA schemes continue to expand coverage, making account-to-account transfers increasingly viable for online businesses.

Payment diversification is no longer optional — it’s strategic risk management.

FAQs

Are open banking payments cheaper than cards?

In most cases, yes. They remove interchange and scheme fees, reducing total processing costs.

Can open banking replace card payments entirely?

For many B2B models, yes. For consumer-heavy e-commerce, a hybrid model may be optimal.

Are open banking payments secure?

They use bank-level authentication and reduce chargeback risk.

Do open banking payments support recurring billing?

Yes, depending on infrastructure and API capabilities.

How fast are SEPA Instant transfers?

They typically settle within seconds, 24/7.

Final Thoughts

Card networks built the foundation of online commerce — but cost structures are increasingly scrutinized.

Open banking payments offer:

- Lower fees

- Faster settlement

- Reduced fraud exposure

- Direct bank connectivity

For euro-based businesses, account-to-account payments are becoming a strategic advantage rather than a niche alternative.

Open a Monetum Account or Talk to an Expert to optimize your payment infrastructure.